Order From Chaos: How Big Data Will Change the World

Harnessing the exponential surge in data creates big opportunities.

Thanks to Purefunds Big Data ETF (BDAT) for helping us put this together. IBM estimates that each day, 2.5 quintillion bytes of data are created or replicated. That’s the equivalent of a million hard drives filling up with data every hour. The current volume of data created is substantial: it is so much that 90% of the world’s data has been created in the last two years. However, the amount of information today pales in comparison to what our future holds, as the rate at which data is created is accelerating exponentially. It’s for this reason that The Economist estimates that there will be roughly 7x more data in 2020 than there was in 2014.

Where Does Big Data Come From?

Big data comes from both internal and external sources. Internally, millions of old documents and records are scanned and archived by businesses. Most of the time, no detailed analytics have ever been run on this information. Externally, the public web offers millions of data sets published for public consumption by government, economic, census, and other sources. There’s also a broad spectrum of data that exists that can be a part of both of these categories: social media posts, documents, emails, business applications, machine log data, media, and sensor data can all be collected, processed, and analyzed. To get a sense of the extent of this information, here’s what is created every hour just from social media and email: 72 hours of video uploaded to Youtube, 4 million search inquiries on Google, 200 million emails sent, 2.5 million shares on Facebook, and 300,000 tweets made.

Big Data = Big Opportunities for Business

With proper analysis, Big Data can lead to new understandings of consumer behaviour, better management decisions, new innovations, and improved risk management. However, there are big challenges in making use of so much information.

Too much data creates an information overload. Organizing and storing all of this data can be problematic. Companies don’t know how to use all of this data to create insight.

To organize and make sense of it all, data scientists use the three V’s to describe Big Data. Volume is the scale at which data is created, and includes the massive amounts of information derived from phones, internet users, machine logs, and internet of things. Velocity is the analysis of streaming data: for example, modern cars have 100 sensors that monitor different systems in real-time. Variety is the different forms of data, and it reflects the fact that data comes in all shapes and forms. Finding a way to harmonize multiple types of data can be quite a challenge. Research finds that organizations spend up to 80% of their time modelling and preparing data, rather than actually gaining insight. Let’s see how companies have been able to use Big Data to create opportunity.

Case Studies of Big Data

Macy’s adjusts pricing in near-real time for 73 million items based on demand and inventory. American Express developed predictive models that analyze historical transactions and 115 variables to forecast the loyalty of customers. Using this data, they can see if customers may be potentially closing their accounts in the near future. Launching a pilot program in Australia, the company can now identify 24% of accounts in the country that will close in the next four months. Walmart built a new search engine for their website that includes semantic data relying on text analysis, machine learning, and even synonym mining to create better search results. Online shoppers have been more likely to complete purchases as a result by 10% to 15%, increasing revenue by billions. Los Angeles and Santa Cruz police departments have used an algorithm that is typically used to predict earthquakes, now using it to look at crime data. The software can predict where crimes are likely to occur down to 500 square feet. In areas the software is being used, there has been a 33% reduction in burglaries and a 21% reduction in violent crimes.

Big Market

Today’s data centers occupy the land to equivalent to almost 6,000 football fields. By 2020, the amount of digital information is expected to increase exponentially to more than 7x of what it is today. In healthcare alone, Big Data is expected to eventually save $300 billion per year in healthcare analytics. Retailers may increase margins up to 60% through Big Data analytics. “Information is the oil of the 21st century, and analytics is the combusion engine.” – Peter Sondergaard, Gartner Research.

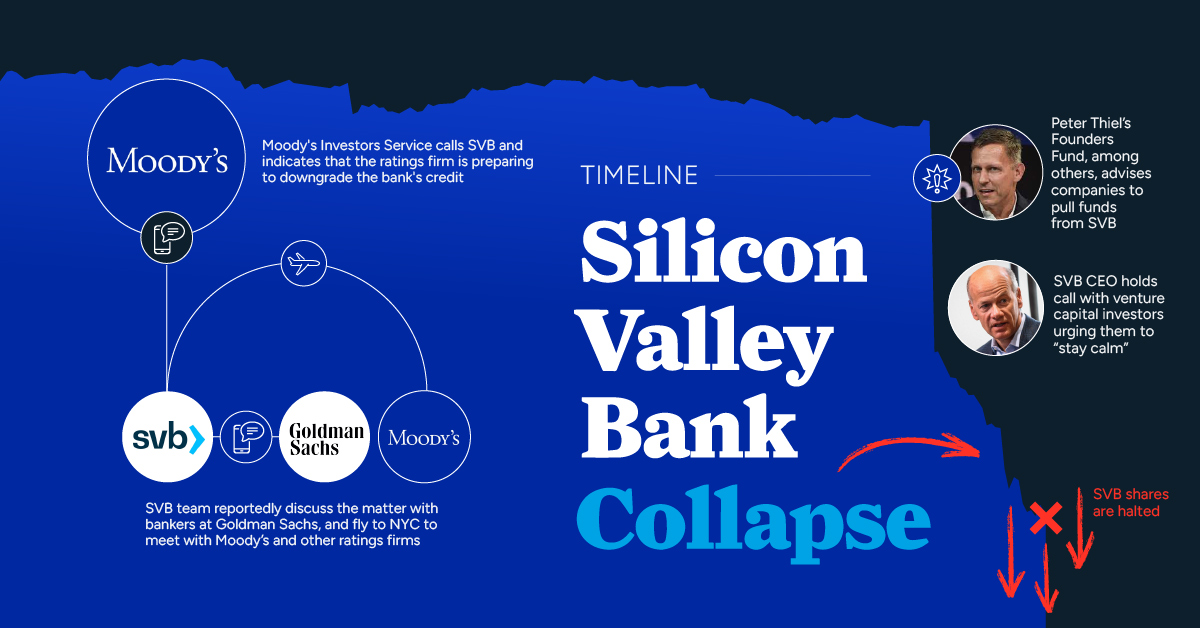

on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

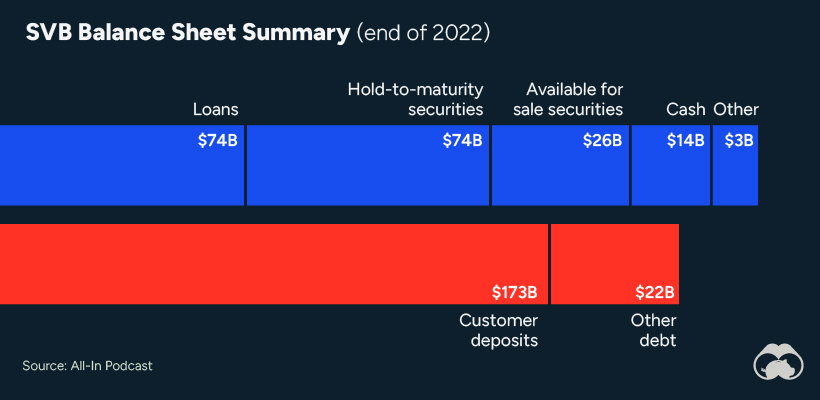

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.